Psychedelic Bulletin #121: The State of Psychedelic Economy and Industry; Dispatch from Horizons New York 2022

This Week:

- 🐜 A smattering of psychedelic company news

- 🗽 Dispatch from Horizons New York 2022

- 💬 Slides & Discussion: The State of Psychedelic Economy and Industry

and more…

Psychedelic Sector News

Psychedelics Company News

- Algernon Pharmaceuticals enters clinical trial agreement with Yale University | Vancouver-based psychedelic drug developer Algernon has inked an investigator-initiated clinical trial agreement with Yale for a Phase 2 study of DMT for depression. Prof Deepak Cyril D’Souza will be principal investigator. In June (Bulletin #106), we reported on a study, led by D’Souza and colleagues, that investigated the safety, tolerability and efficacy of DMT in a typical hospital setting. The explorator study provided support for DMT’s potential rapid antidepressant effect.

- atai’s Perception Neuroscience completes enrollment for Phase 2a trial of R-Ketamine for TRD | The company expects to share topline results around year-end 2022. Indeed, much of atai’s investor-fcused R&D day was spent teasing the upcoming results.

- Psylo raises $5m for psychedelic drug discovery | Read our interview with CEO Josh Ismin to learn more about the Aussie biotech.

Featured Psychedelic Jobs

- Psylo is hiring a VP of Drug Development.

- PsyMed Ventures is looking for a full-time Ops Associate.

Browse more roles and get more job posts to your inbox by signing up for alerts here.

Weekend Reading

Dispatch from Horizons New York 2022

Words by Josh Hardman

We were pleased to once again be in attendance at Horizons: Perspectives on Psychedelics in New York City; and very proud to be Media Sponsors for this year’s event, along with our friends at Psychedelics Today and Lucid News.

Amidst a swelling crop of for-profit psychedelics conferences and industry events, Horizons has a certain ineffable authenticity to it. This year marked the 15th annual conference, a milestone on which the organisation’s founder, Kevin Balktick, took time to reflect at a small gathering on the final night of the four-day assembly. Long-time Horizons attendees told me that early gatherings were hosted in a church, with little more than a coffee urn at the back of the room and a decidedly ‘underground’ feel.

While other conferences now feel more like trade shows, Balktick has managed to maintain many elements of a more ‘psychedelic’ or academic atmosphere, while ensuring the viability of the annual conference. Keen to encourage a similar ethos at similar events, yesterday Horizons shared some key guidelines that other psychedelic conferences organisers might adhere to.

In terms of the programming, this year’s conference had a varied offering once again. Thursday hosted the second Psychedelic Business Forum and a number of workshops and classes, with the remaining days tackling Psychedelics in Research, Medicine, and the World.

The Great Hall at The Cooper Union once again provided the impressive venue for the majority of proceedings, while the Psychedelic Business Forum, and a number of classes and workshops, took place at the New York Academy of Medicine. Both buildings have interesting architectural and historical import (see last year’s Dispatch).

One of our highlights of the conference was the manner in which many researchers chose to share both quantitative and qualitative data from their studies. All too often, researchers focus on the former when presenting their results, showing graphs depicting data such as endpoints and statistical significance. While this is of course of great importance, it can obfuscate the rich personal experiences that might hint at how these impressive therapeutic outcomes are achieved.

We were especially pleased, then, to see how Michael Bogenschutz and Gabby Agin-Liebes shared both quantitative data but also qualitative patient experiences when discussing psilocybin-assisted therapy for alcohol-use disorder. Bogenschutz began by sharing the more quantitative findings (which we analysed in Bulletin #117), and then Agin-Liebes shared a number of powerful excerpts from patient experiences. These individual qualitative data points are also amalgamated to identify shared trajectories of healing throughout the trial, mapped onto the buckets of awareness, intrapersonal and interpersonal beliefs.

Immediately after their presentation, Manish Agrawal and Paul Thambi of Sunstone Therapies took to the stage to share their work on psilocybin-assisted therapy in end-of-life and palliative care. Once again, the presentation was a compelling blend of historical and quantitative datapoints, along with excerpts from patient experience reports.

There were so many presentations worth sharing at Horizons that we couldn’t possibly begin to write them up here. Thankfully, recordings will be made available in due course. At that time, we will share some of our favourite presentations in the Bulletin.

Slides & Discussion: The State of Psychedelic Economy and Industry

At Horizons New York 2022, I had the pleasure of opening the second Psychedelic Business Forum. I was tasked with providing an overview of psychedelic business, including a look at the past 12 months and some forward-looking analysis.

The slides I ended up preparing could have sustained a 2-hour talk, but thankfully the organisers spared the audience and gave me 30 minutes to hop and skip through my presentation.

For those who couldn’t make it, here’s the full slide deck.

Now, it’s quite image and data heavy, so flipping through the slides alone might not be too useful. So, I decided to provide a very rough annotation of the slides below.

I give more attention to some slides than others in the writeup below, so if there’s something you would like me to explain further, just reach out.

The unofficial title of my talk: What’s all this Psychedelics Business?

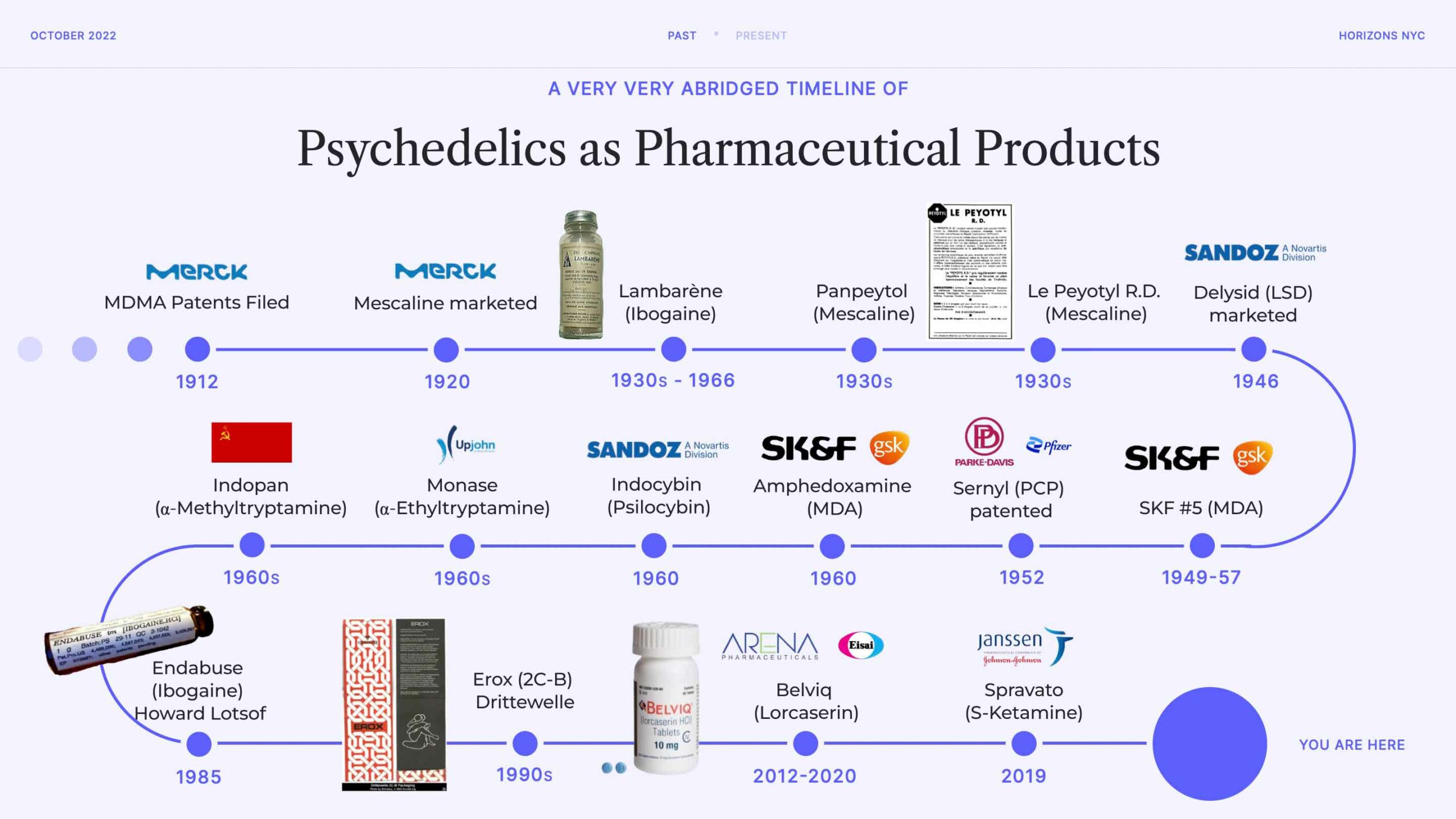

I decided to ground my presentation on ‘psychedelic business’ with a little historical context. So, the first couple of slides provide some abridged timelines of psychedelics as pharmaceutical products, and the third looks at mid-century psychedelic-assisted therapy offerings.

Here is a very, very abridged timeline of instances where psychedelics (and related molecules) have been marketed as pharmaceutical products: both in prescription and more ‘retail’ instances.

Now, it’s important to know that the meaning of the word “marketed”, in this context, has changed over time. Prior to the thalidomide tragedy and the ensuing institution of a strict clinical trial regime in the U.S. and elsewhere, practitioners were able to ‘try out’ drugs with little oversight. When it came to psychoactive drugs this experimentation took place in myriad settings of varying ethical quality: from the involuntary dosing of inpatients at mental health facilities, right through to voluntary (and even for-profit) LSD-assisted therapy among the elite (more on that later).

With that said, this slide features a number of well-known ‘big pharma’ companies, from Merck and Sandoz through to GSK and Pfizer. Of course, in many cases the entity exploring psychedelics in the 20th century has been acquired, as in the case of Smith, Kline & French (now part of GSK). Companies like Merck and Sandoz were dishing out their formulations of drugs like mescaline, LSD and psilocybin in the hopes that researchers and practitioners might find a commercially viable use for them.

Aside from this less-focused approach to discovering uses of psychedelics as pharmaceutical products, there were also more concerted drug development efforts. U.S. pharmaceutical company Upjohn marketed its first CNS drug in the 60s: an antidepressant under the name Monase. The drug, α-Ethyltryptamine, was ultimately withdrawn. Interestingly, the former Soviet Union (USSR) developed α-Methyltryptamine for the same purpose, and marketed it as Indopan (not to be confused with a more recent anti-inflammatory drug of the same name). The decision to pursue differing analogs for the same indication was interesting to me, and reminded me of just how much the U.S. and Russia differ in their pharmacopoeias.

There are also some interesting cases of more “over the counter” (note: I’m using this in the UK sense of the phrase, whereby a product can be purchased without a prescription) incarnations of psychedelics in the 20th century. Formulations of ibogaine and mescaline were available from the 1930s, with one mescaline product, Panpeyotl, originating from Cote d’Azur and available via mail-order.

Another mescaline product, Le Peyotyl R.D., was advertised in France as ‘one of the best natural tonics’ and the ‘surest weapon against pain’. The indications listed are broad—including asthenia, depression, migraines, hysteria and irritating cough—but generally revolved around lack of energy and weakness. Through my dodgy French language and currency translation, it looks like a week’s supply would set you back around $25 in today’s money. See page 25 of this UN Bulletin on Narcotics publication to review the handbill for this curious product.

There’s lots more to discuss—including the many cases that didn’t make it to this slide (such as ergolines) and the edge cases like Lorcaserin—but I, regrettably, don’t have the time to do so here.

Those who are interested in these histories should consult the true experts on the topic. These include Ericka Dyck, Mike Jay (who has a new book coming soon), Matthew Oram, etc.

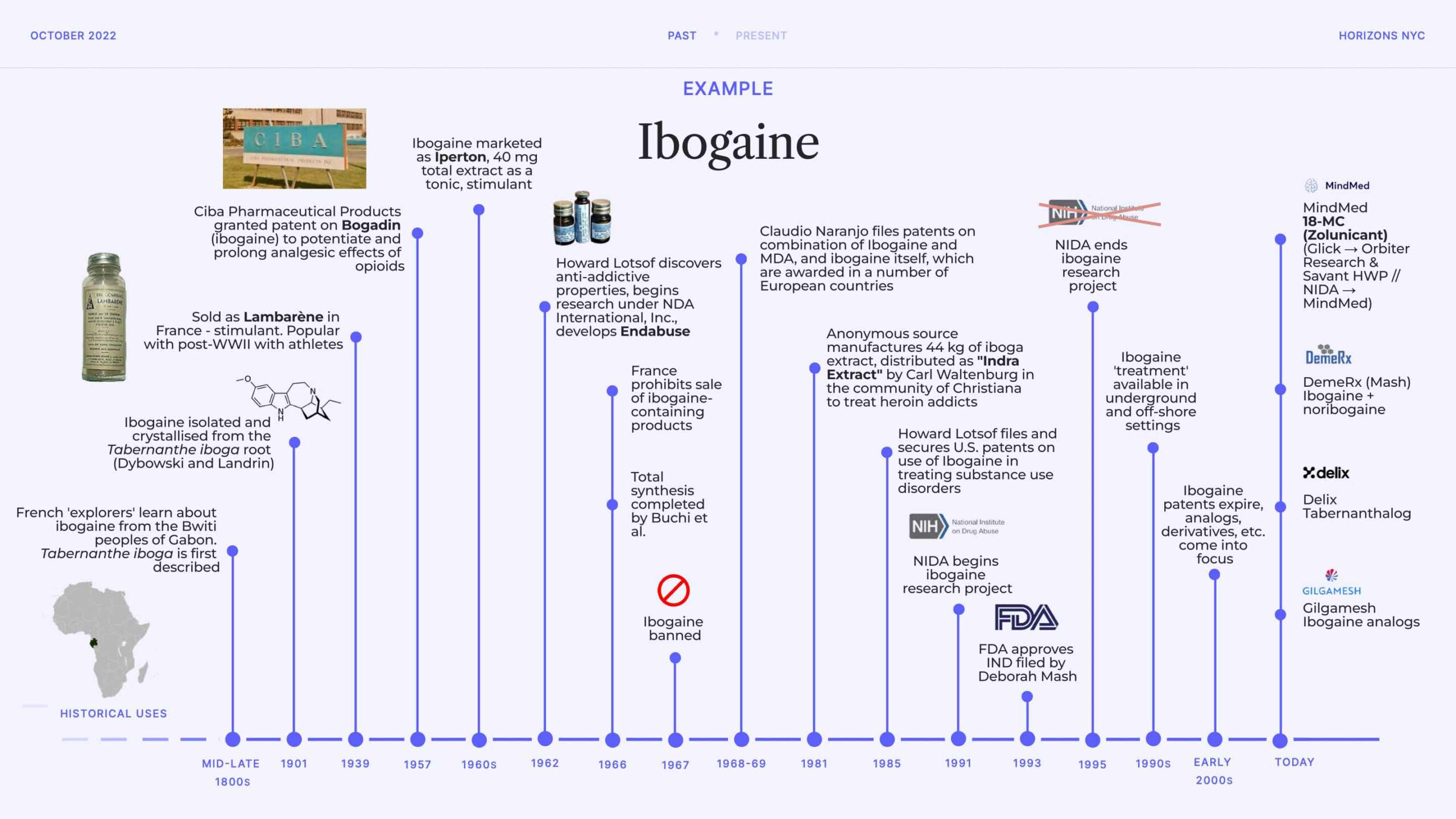

I decided to pull focus on one psychedelic (admittedly an atypical one) to show how, despite over a century of interest from business actors, the type of drug development activity we are seeing today is certainly different in character.

I won’t narrate this slide here, as it’s quite self-explanatory. I will note that it again excludes many data points; not least the interesting recent regulatory histories of ibogaine in countries like Canada and New Zealand.

The main point of this slide is to show that today there is a great deal of interest in developing ibogaine analogs and derivatives, as opposed to ibogaine itself (with some notable exceptions, such as Deborah Mash’s DemeRx). I suggest that this likely has something to do with the safety profile of ibogaine, but also the fact that many of the original patents pertaining to its use in prominent substance use indications, and even analogs like 18-MC, have generally expired or are nearing expiration.

This is a more generalisable observation across today’s psychedelic drug discovery and development landscape: a tilt toward analogs, derivatives and deuterated forms. Of course, some of this tinkering might lead to safer and more efficacious drugs, but there are certainly groups who are developing NCEs for the sake of it (where “it” equals IP and fundraising prospects).

There are a couple other interesting points on this slide that I noted during my talk, such as the Lambarène formulation of ibogaine which became popular with post-WWII athletes in France and beyond. There are fascinating accounts of expeditionists and climbers popping Lambarène to maintain progress and more generally for those embarking on ‘physical or mental efforts’. There were also instances where it was used in more mundane settings to help with fighting fatigue and depression, among other indications. Ibogaine was later marketed as Iperton, with similar tonic and stimulant use cases suggested.

The next major wave of interest is sparked by Howard Lotsof, who stumbles upon the apparent anti-addictive properties of the drug in 1962. This sparks a lifelong passion for Lotsof, who incorporates NDA International, Inc. to fund research. He came up with the straightforward name, Endabuse, for his ibogaine product in development. Of course, the research environment gets trickier after ibogaine is made illegal in many jurisdictions in the late 1960s, though a number of researchers and advocates (both underground and above board) continued to explore its potential to alleviate substance use disorders (such as Carl Waltenburg’s efforts to distribute iboga extract in Freetown Christiana, the semi-autonomous commune in Copenhagen). Above board, Deborah Mash is widely considered to be the torch-carrier of modern ibogaine research, which began when her IND was approved by the FDA in the early 1990s.

Now, the last couple of slides largely focused on the drugs alone, but that overlooks the fact that psychedelics were also being explored in the container we generally see them being developed in today: psychedelic-assisted therapy. In this context, the drug is viewed as a catalyst to more conventional therapy.

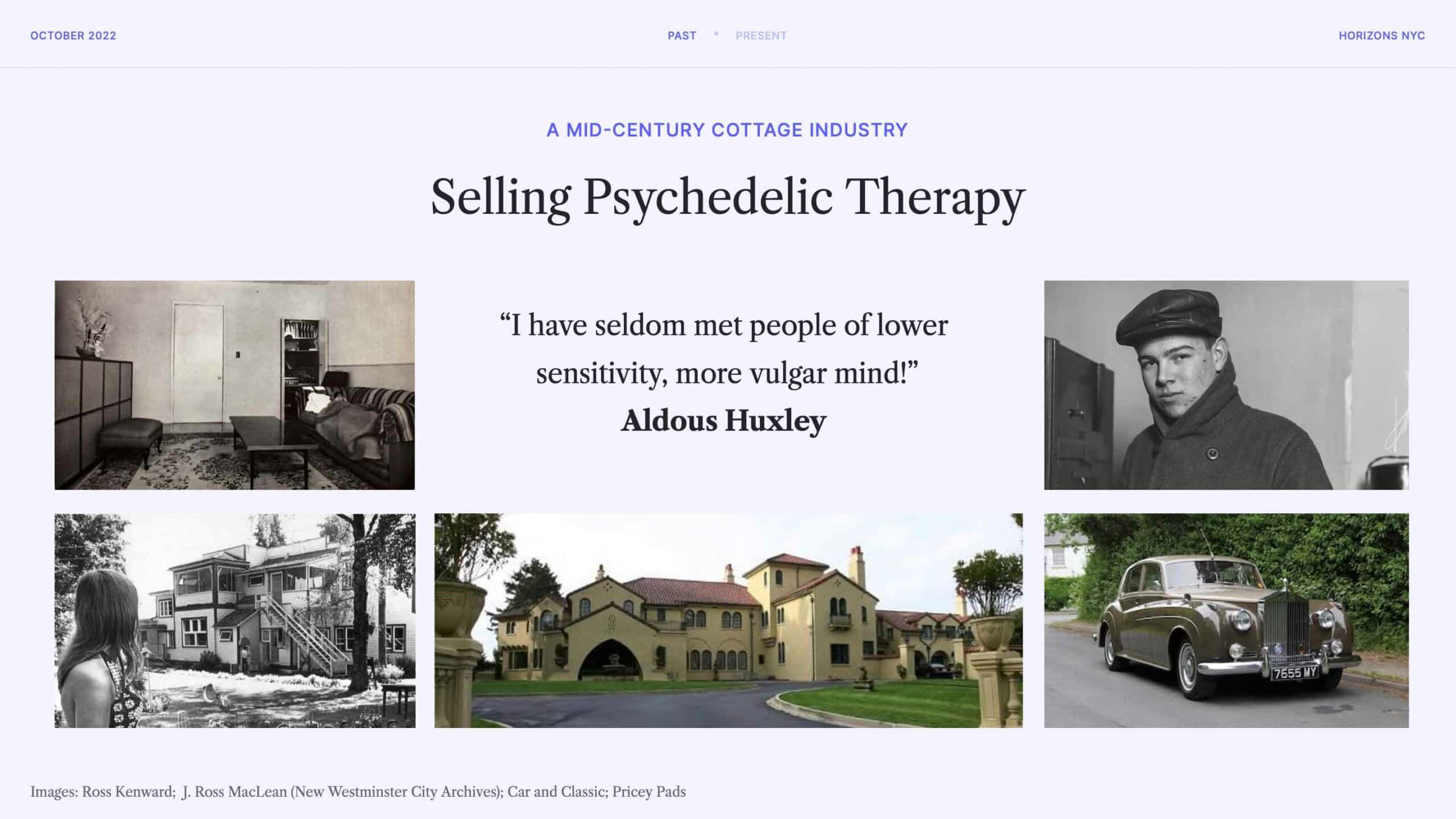

This certainly existed as a business in the mid-20th century (I didn’t cover the underground in this presentation; this was generally happening above board), with some entrepreneurial folks making quite a profit.

This slide shows images of The Hollywood Hospital (Vancouver, not LA) which was founded by J. Ross MacLean and Al Hubbard. They would charge patients up to $1,000 for LSD therapy, which is around $10,000 in today’s money, and remember that these types of set-ups were often getting the LSD from Sandoz for free (or thereabout). Clients of these types of services included the likes of Cary Grant and Betsy Drake. See Montecristo Magazine’s history for more.

Aldous Huxley had something to say about these types of set-ups, as you can see.

Okay, that’s the mini history safari over: onto the present day. My first few slides set out to define “Psychedelic Business” and provide an overview of recent funding activity.

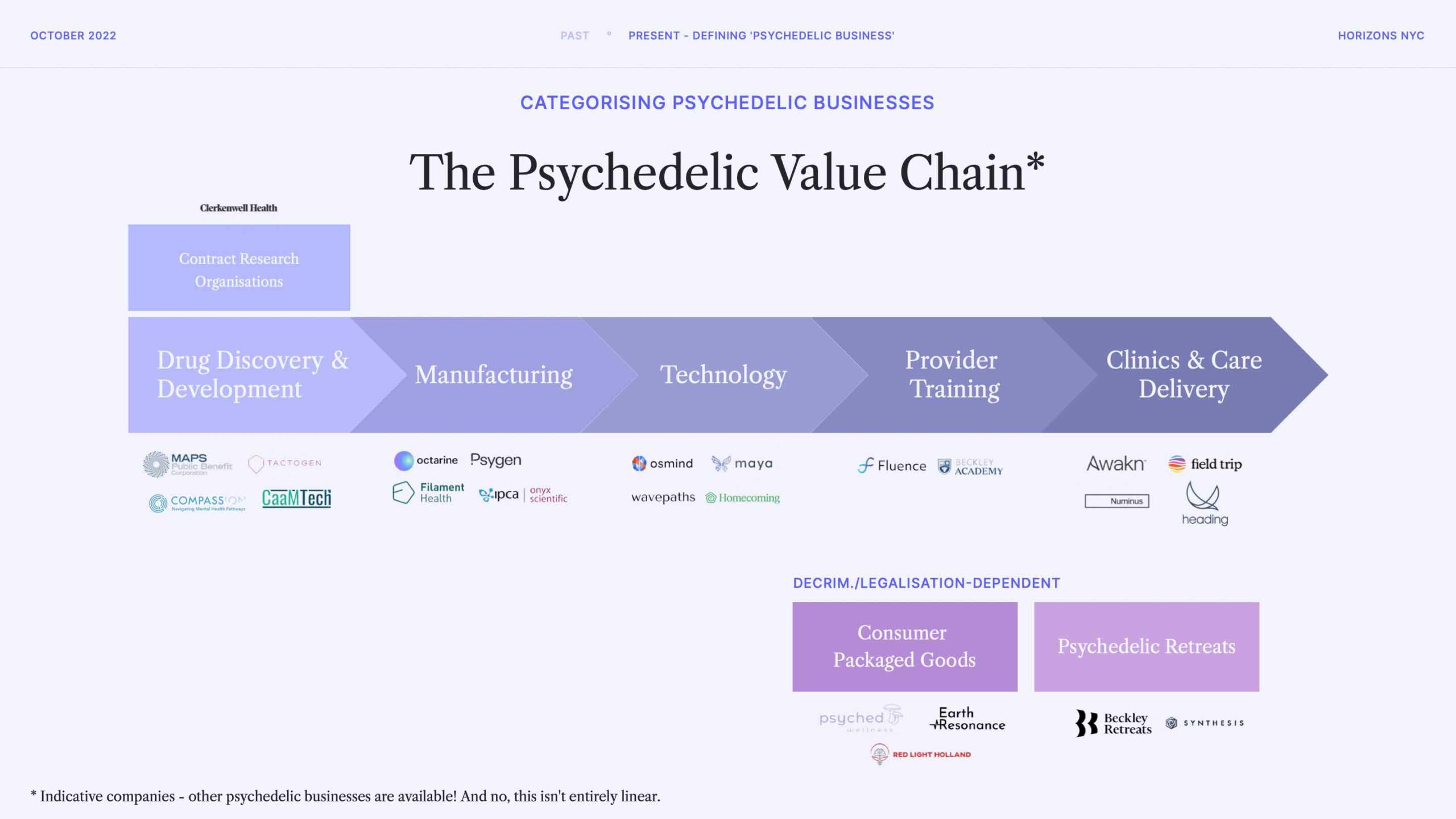

So, first things first: what do psychedelics companies actually do? The easiest way to show this is by visualising companies along a value chain. There are many ways of splicing these segments, but we found this to be the most useful.

We focus on companies operating legally, with some limited focus on those operating in grey areas or regionally-legalised markets. You can see those types of segments in the bottom portion of the slide.

The bulk of our focus, then, is shown in the value chain, which is not entirely linear.

Of course, there are many other ways of mapping psychedelics companies and their activities. For example, we have previously visualised companies along the patient journey view (we have not published this work), which is especially useful when considering tech companies in the space.

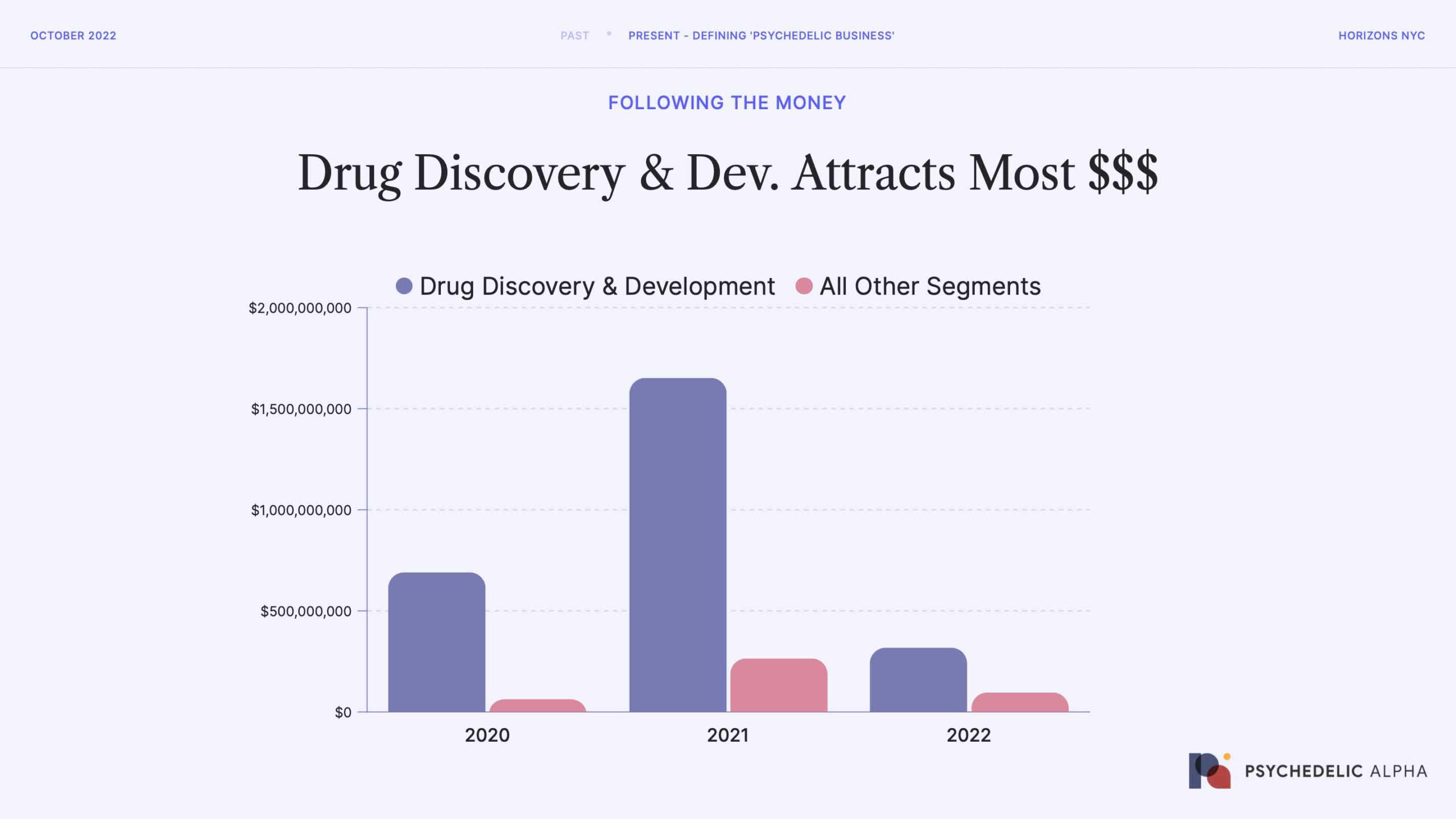

This chart tells a pretty simple story: almost all of the money invested into psychedelics companies is accruing to the drug discovery and development portion of the value chain. This should be unsurprising: both because of the capital intensity of drug development, but also due to the emergent nature of psychedelic drug dev. (not a single candidate has been approved, unless we include esketamine).

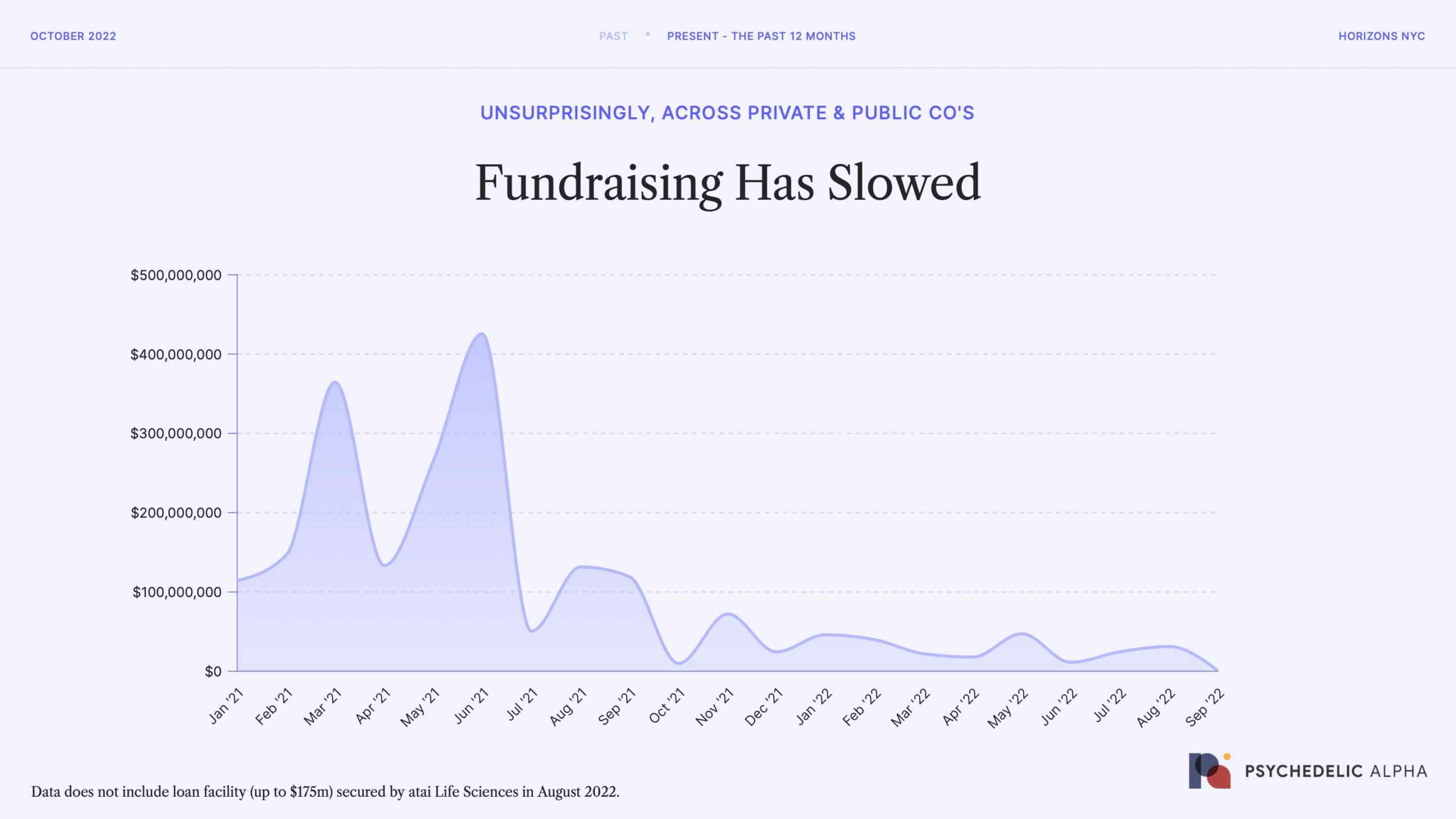

The other obvious trend here is just how significantly fundraising has declined in the past year.

Source: Psychedelic Alpha data, which captures both public and private fundraising.

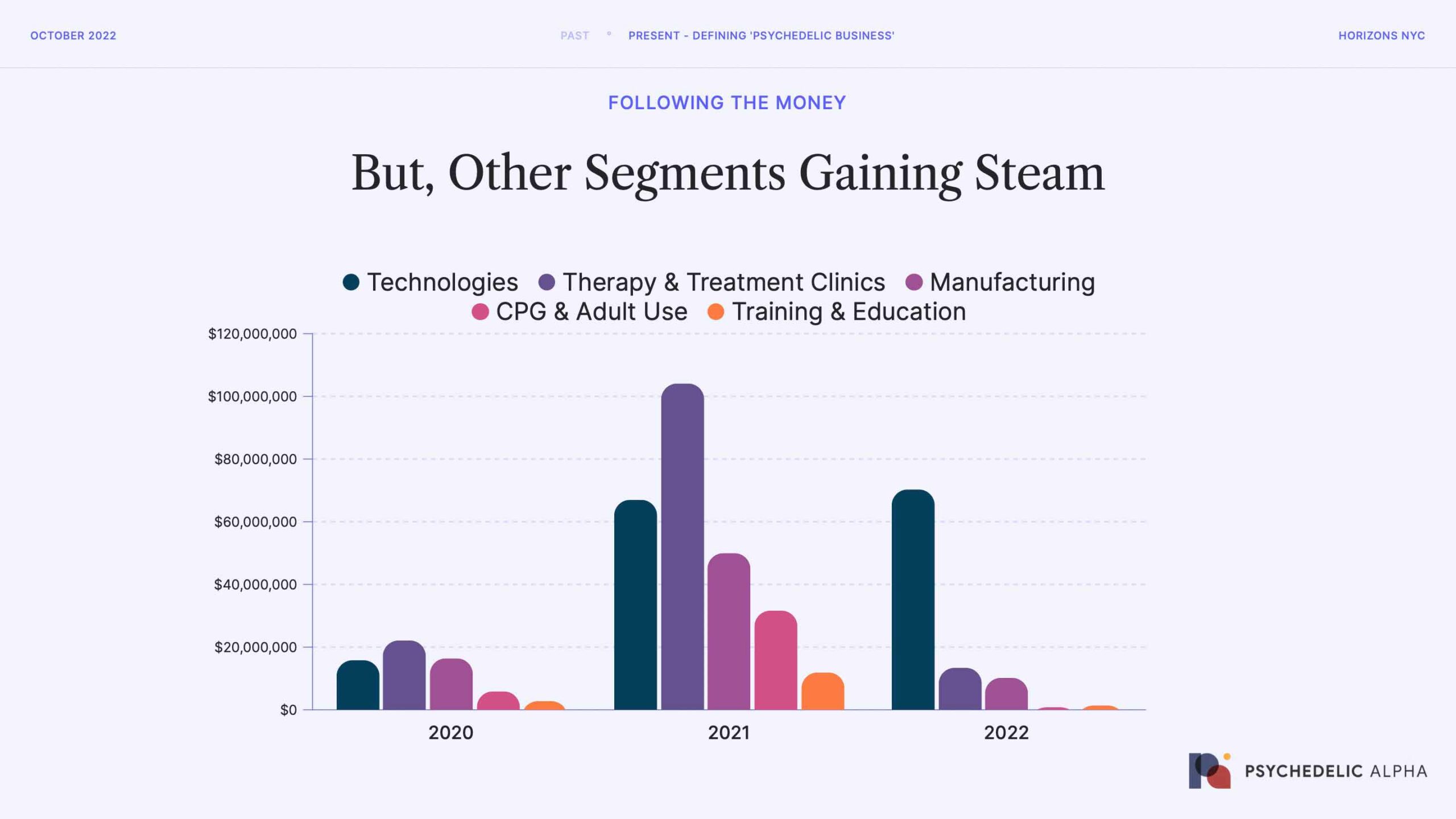

Now, let’s break down those “Other Segments” from the last chart to see where money is flowing besides drug discovery and development.

Technologies for psychedelic therapy (think niche apps and EHRs) are a clear area of interest that’s maintaining steam in 2022, with fundraises like Osmind’s $40m Series B demonstrating investor support. Psychedelic manufacturing was relatively popular last year, too, but has since cooled off.

Remember, though: the amount of money invested in all of these segments is still very small compared to drug discovery and development.

Source: Psychedelic Alpha data, which captures both public and private fundraising.

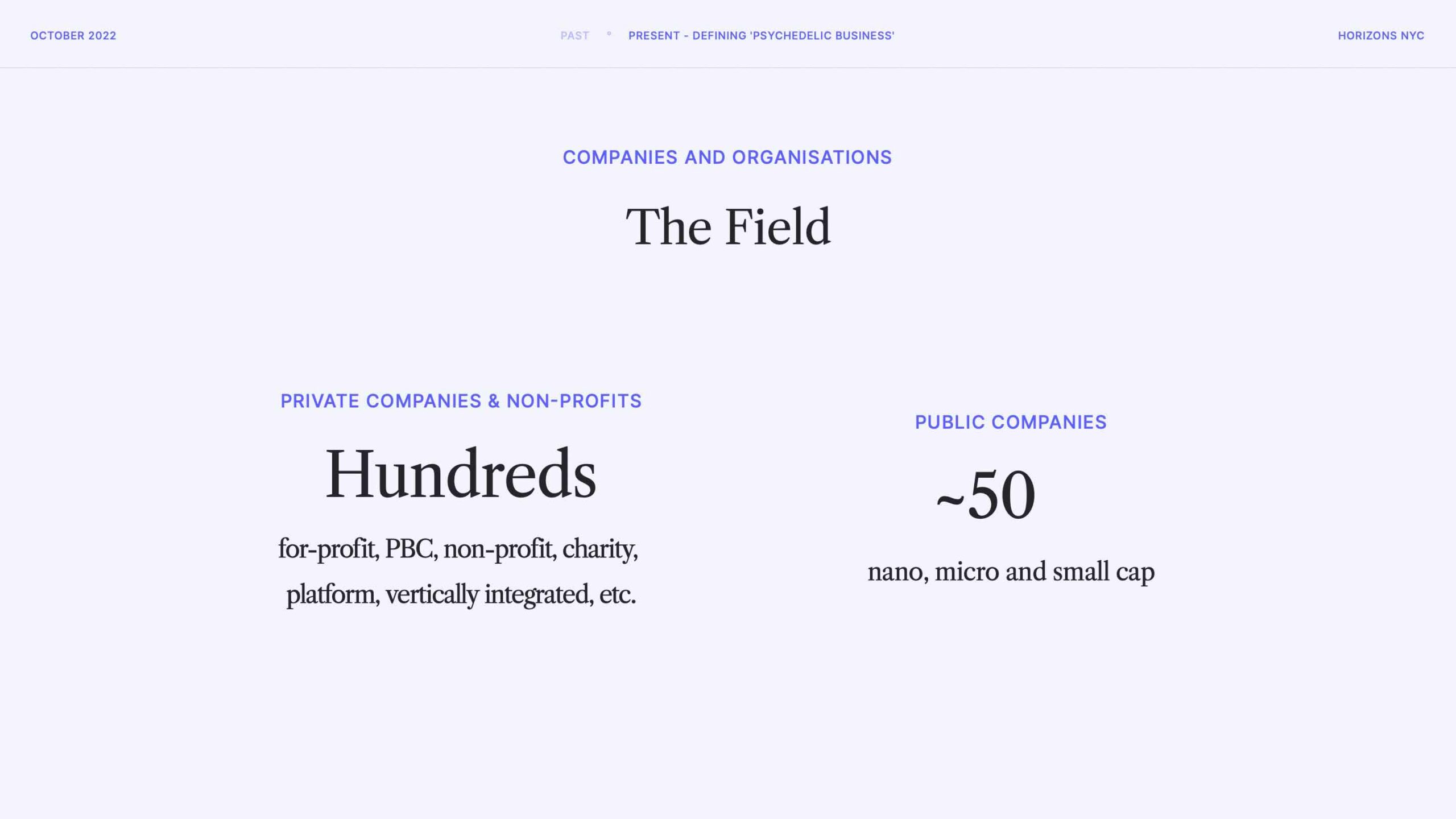

This funding, as well as philanthropy not captured in the aforementioned data, is sustaining hundreds of ventures, around 50 of which are public.

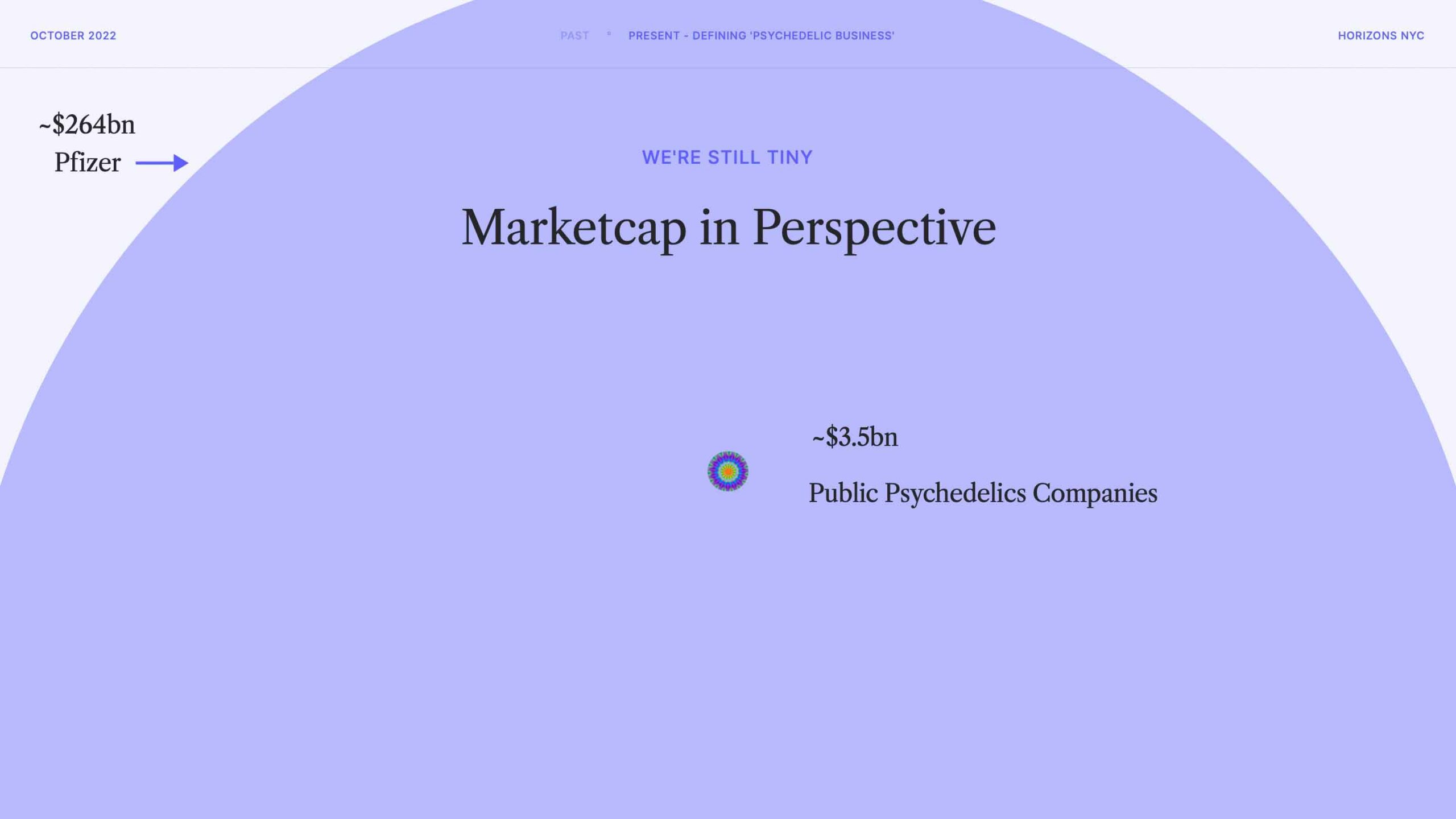

We often focus on public companies when it comes to reporting on the financial and commercial health of psychedelics companies. The main reason for that focus is reporting requirements, which allow us to get a look under the hood at drug pipelines, cash burn and other operational commentary disclosed in filings.

When taken together, the market cap of all public psychedelics companies was around $3.5bn when these slides were originally compiled. That’s just over 1% of the market cap of just one ‘big pharma’ company, Pfizer. It’s early doors.

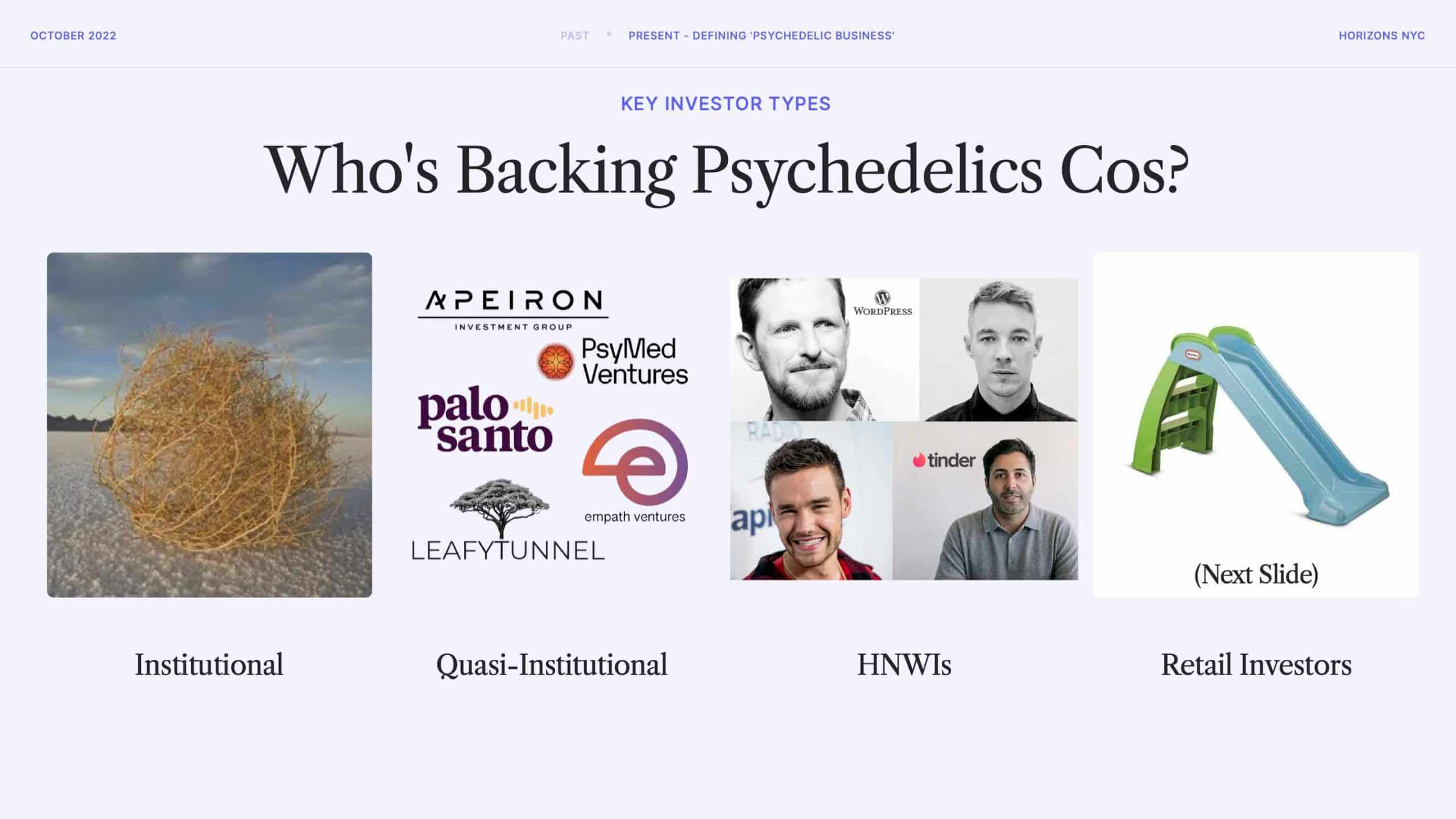

Given how nascent the psychedelics market is, who’s backing psychedelics companies?

Well, institutional investors are largely absent, except for a few limited cases. It’s predominantly what I sloppily refer to as quasi-institutional investors: think psychedelic VCs and family offices. These folks are, thus far, driving the majority of investment in early-stage psychedelic companies, at least in the private markets. They’re joined by a curious coterie of high net worth individuals which includes the likes of WordPress founder Matt Mullenweg, One Direction’s Liam Payne, and the DJ and music producer Diplo.

Once psychedelic companies go public, though, retail investors become significant shareholders.

We compared the ownership characteristics of 9 representative psychedelics stocks to those of 9 pre-revenue biotech comps, and the results were striking. Psychedelic stocks have an enormous level of retail ownership, which might go some way to explaining the chop we have seen in the markets. It could be argued that many retail investors aren’t in for the long haul, which is important when investing in risky assets like biotech.

Now that we have an overview of what psychedelic businesses are and the fundraising environment over the past few years, let’s focus on the last 12 months.

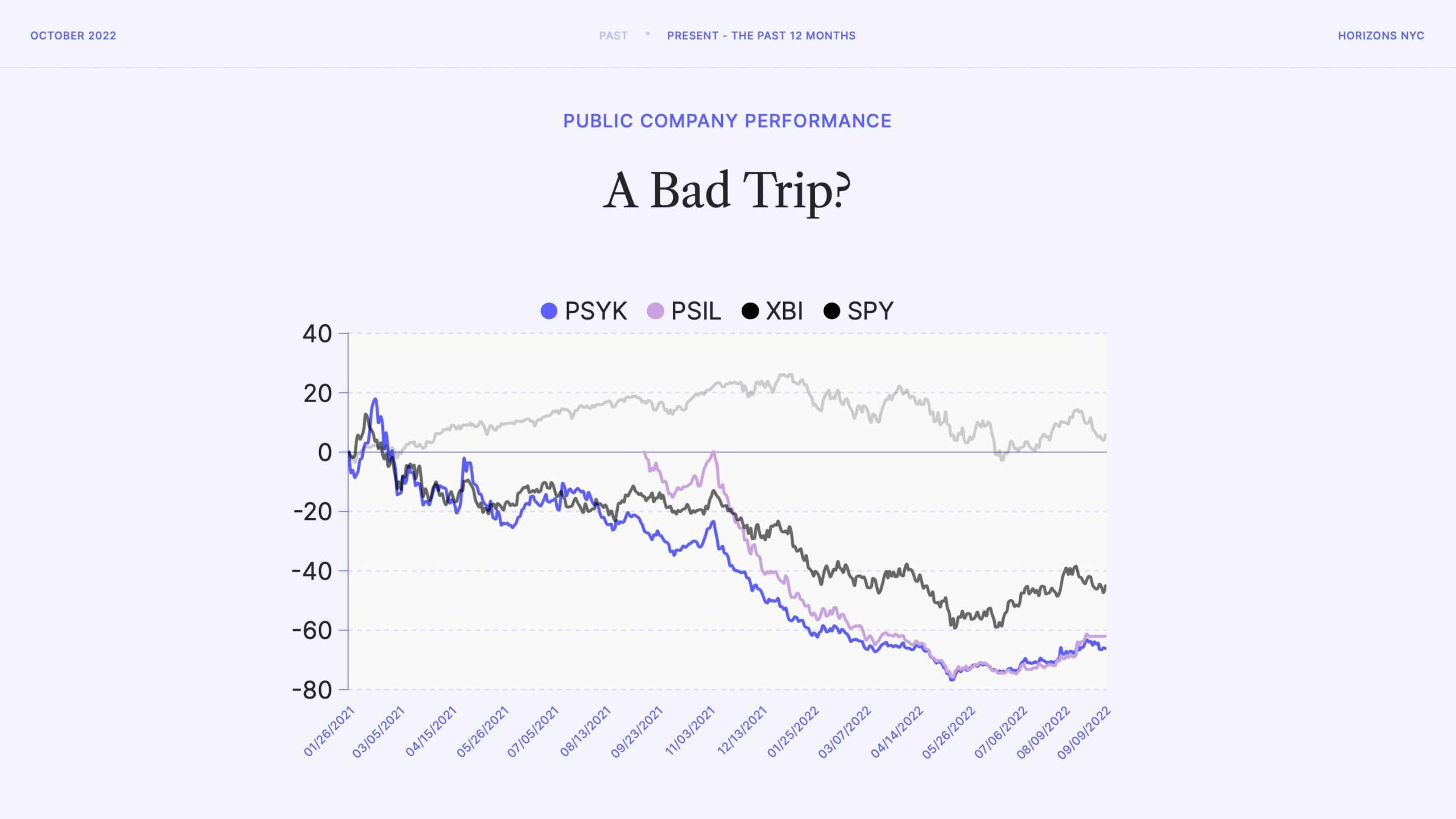

It’s been a bad trip for investors in public psychedelics companies, with stock prices slipping over 90% in some cases. Some of this is macroeconomic, as the S&P 500 (SPY) has also struggled in the past year. The biotech industry has taken a beating more broadly, too, with the S&P Biotech Index (XBI) showing losses of up to 60%.

But, as is clear from this graph, psychedelics stocks (shown here using the psychedelic indexes PSYK and PSIL) have underperformed even the biotech market.

But, that’s just the public markets; and they’re renowned for being choppy.

So, we revisited our in-house fundraising data to see what’s happened since January 2021. As you can see, the first three quarters of three quarters of 2021 were robust, but things cooled off around a year ago when the fundraising environment bottomed-out in October 2021. Since then, it’s been comparatively sluggish, with fundraising remaining low throughout 2022.

Source: Psychedelic Alpha data, which captures both public and private fundraising. Do note that this graph excludes a loan facility secured by atai Life Sciences in August 2022.

Despite this gloomy financial situation (and outlook), investors appear to remain optimistic.

According to our Summer 2022 Psychedelic Investor Pulse Survey, the majority of psychedelic investors in our community remain largely positive. What was most striking from this survey is that the larger, quasi-institutional investors were the most optimistic, and demonstrated the most staying power.

Of course, this apparent optimism and staying power among larger investors could be the result of two factors:

- Investors with ‘dry powder’ are in the driving seat right now, meaning they are able to invest in companies at better terms and lower valuations than last year

- Investors in psychedelics companies have a vested interest in signalling optimism around the sector, so likely over-reported their sentiment in this survey

With this tumultuous twelve months behind us, let’s turn our attention to what we might expect to see in the next 6-12 months.

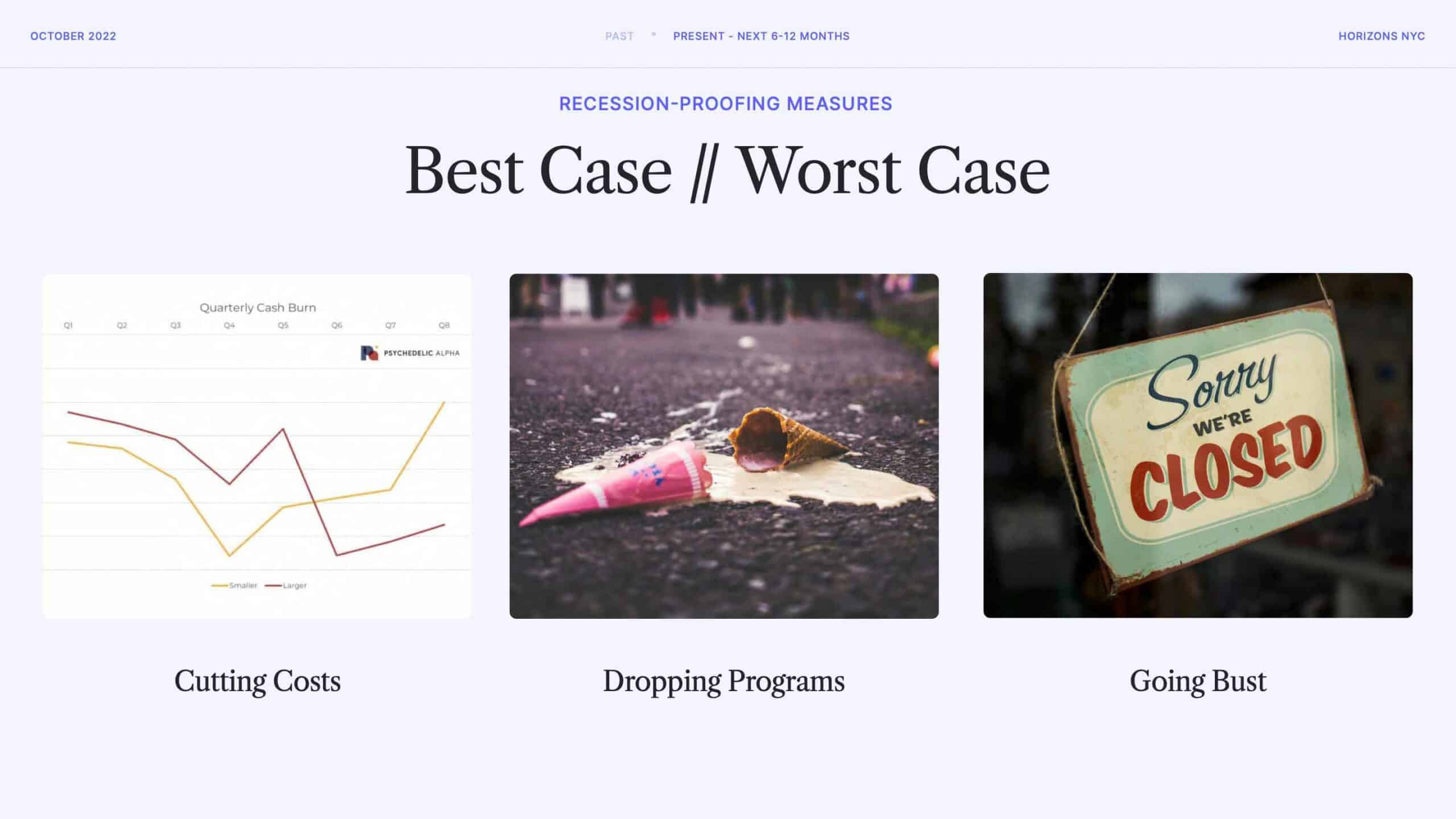

On the business side of things, we should expect to see recession-proofing measures rolled-out across most ventures, especially publicly traded companies.

The most obvious way to weather the storm is to cut costs. In August, we shared in-house analysis that showed the smaller psychedelic public companies were cutting costs at a significant clip, while the largest companies reigned in spending more modestly as they enter later-stage trials.

We should expect to see cost-cutting deepen, especially as around half of all public companies are set to run out of cash in the coming months (many have already).

One major way of cutting costs is by dropping a drug development asset or program. Even the larger psychedelics companies, like atai and MindMed, have shelved candidates. While it’s natural for drug discovery and development companies to concentrate their bets on lead candidates over time, in times of financial strain this only becomes a more immediate focus.

And, for those companies that are unable to reign in their spending or secure new financing, they’ll simply go bust. We have already seen this happen among a handful of publicly traded companies this year, and a number of private ones too. Some of the public companies are turning to less attractive financings, in a desperate attempt to stay solvent. Some of these can be described as “death spiral financings”.

Of course, the flipside is that well-capitalised companies might see this situation as a fire sale, with pipeline assets, programs, and whole companies up for sale at a discount. Look at Beckley Psytech’s acquisition of Eleusis last week, for example.

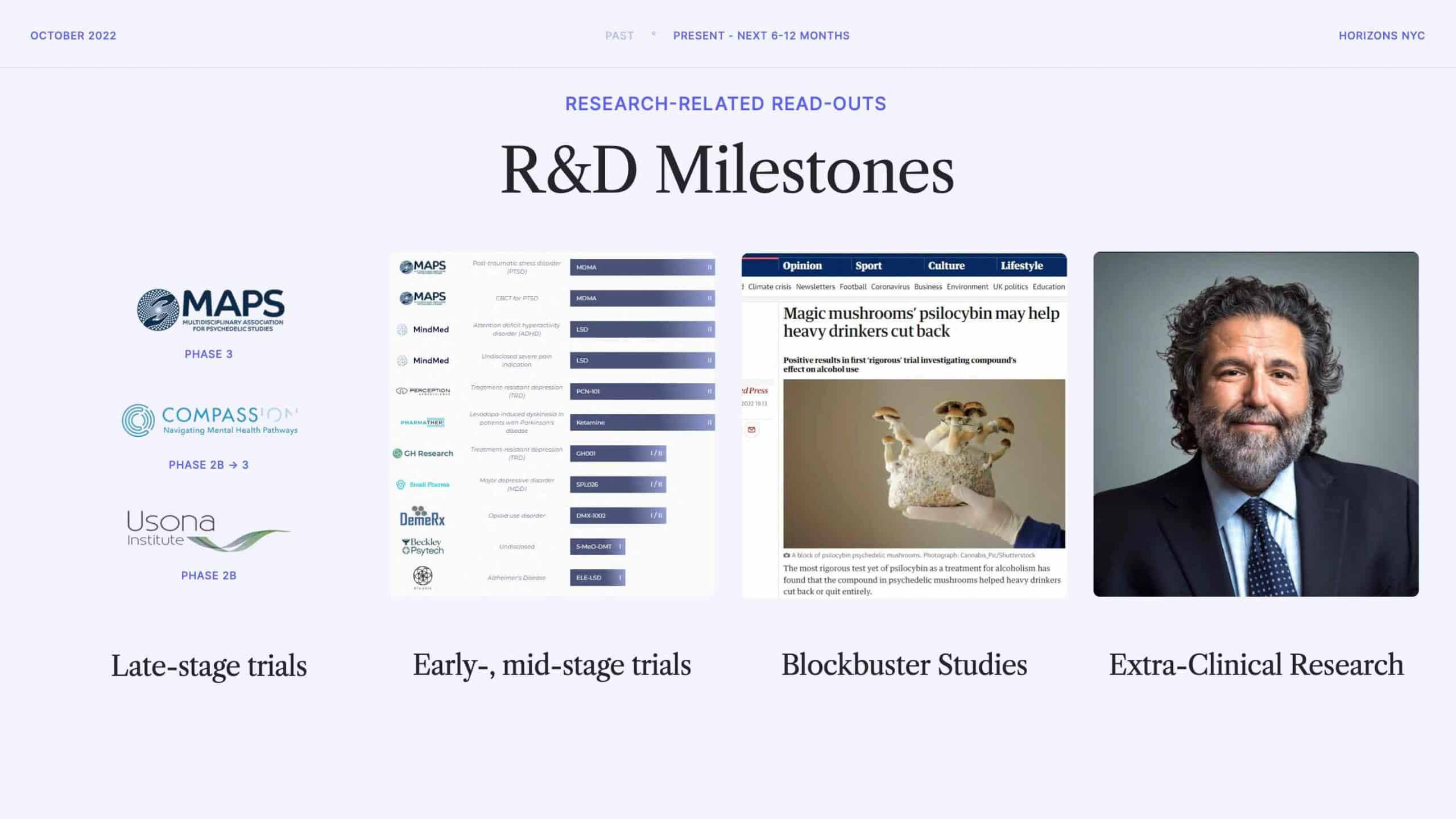

But, it’s not all corporate and financing-related news that we should expect to see in the next 6-12 months. There’s a number of research-related readouts to look forward to.

On the drug development side there are a variety of milestones on the horizon. MAPS is in its second Phase 3 trial of MDMA-assisted therapy for PTSD and COMPASS Pathways is hoping to commence the first Phase 3 trial of psilocybin by the end of this calendar year, to name just a couple of examples.

Behind these later-stage trials there’s a huge number of early and mid-stage trials, as well as a bevy of discovery and preclinical work. This work is captured in our Psychedelics Drug Discovery and Development Tracker, masterfully maintained by Michael Haichin.

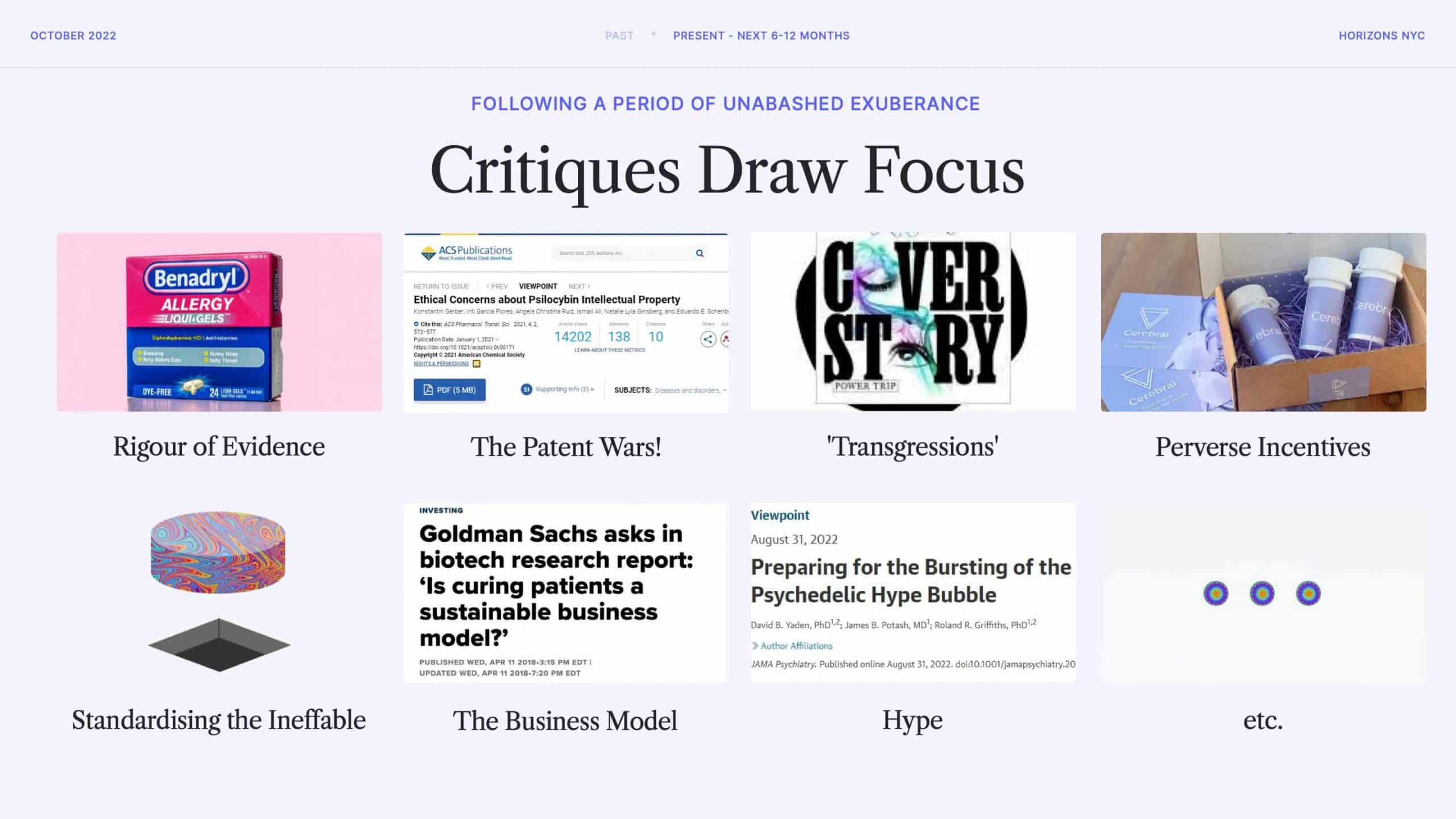

My key question about this large midriff of trials is: how many will actually make it through to publication or any utility, given the financial situation? Clinical trials are incredibly capital intensive, and I can’t imagine the majority of these trials being funded through to completion. Indeed, a cynic might say that many of the earlier stage trials were ‘press release trials’, just like ‘press release patent filings’, that were often geared towards raising funds.

Beyond the financial situation, the IP landscape has changed significantly in the past couple of years, and continues to become apparent. Due to the 18 months of secrecy afforded to patent applicants, it can be tricky for actors in emergent fields to know where they can operate without potentially being cut-off by an unknown patent filing and potential grant. As such, the emerging IP landscape might have significantly disincentivised or effectively precluded some of these trials.

Beyond these sponsored trials, there’s also a great deal of investigator-initiated and ‘academic’ research and trials to look forward to hearing about in the next 6-12 months. Not least of these is the religious leaders study, led by Tony Bossis at NYU (pictured in this slide), which seeks to disaggregate the mystical experience by giving psilocybin to religious leaders of various stripes.

And, we might expect more ‘blockbuster’ studies that draw mainstream attention. A recent example was the psilocybin for alcohol use disorder (AUD) study out of NYU, which was widely reported in the media.

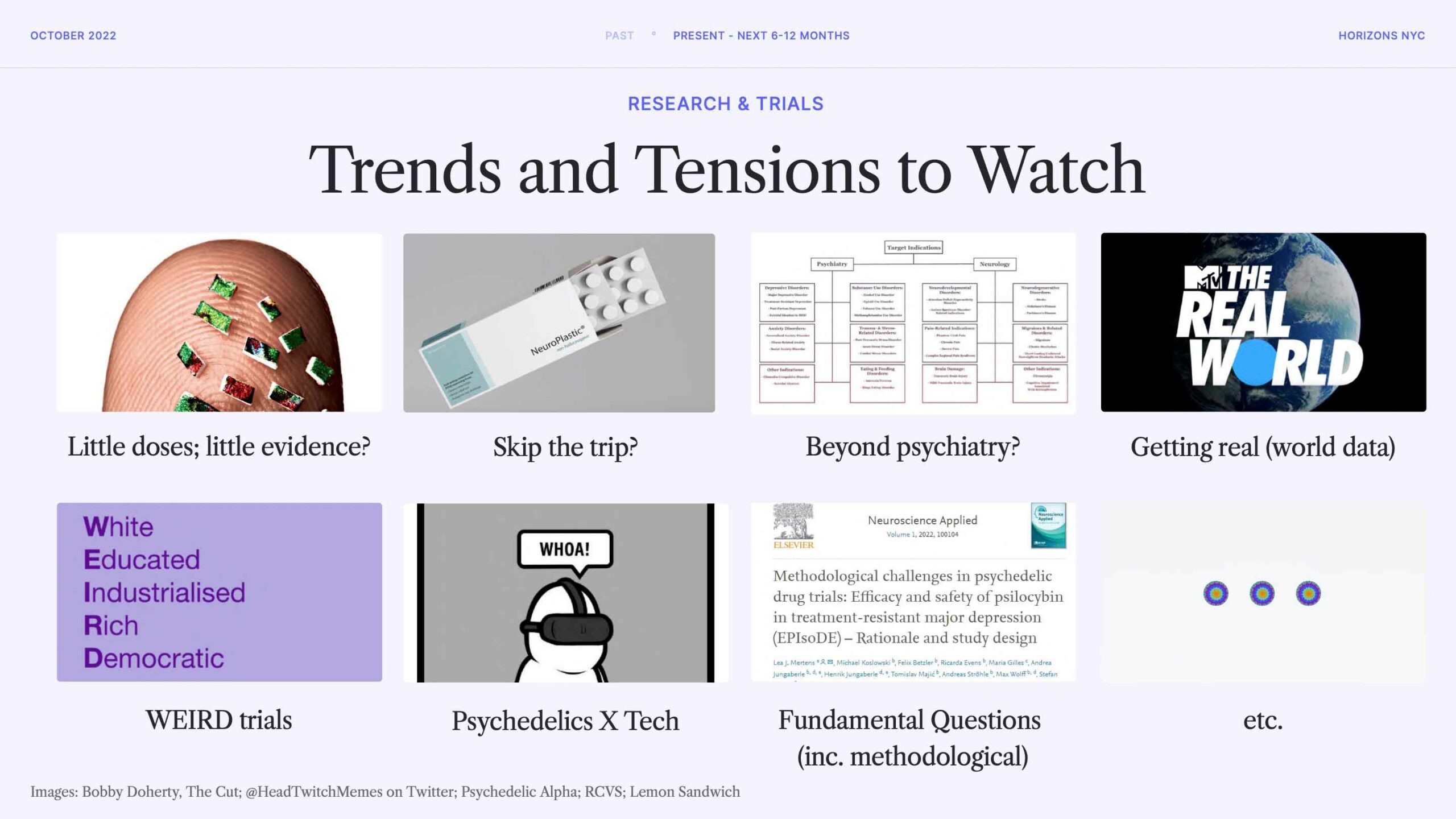

Zooming out from individual trials and research projects, there are a number of trends and tensions that we might expect to see over the next 6-12 months in the R&D arena.

I only had time to touch on a couple of these during my presentation. First was the trend toward exploring the potential of non-hallucinogenic psychedelics (or, “psychoplastogens), which has become an increasingly popular avenue of investigation and investment. I expect this to only continue in the next 6-12 months as these molecules enter the first in-human trials, and the innovative trial methodologies of groups like those at Stanford (Boris Heifets’) and University of Wisconsin share their findings.

I also mentioned the unfortunate trend of WEIRD trials: the fact that clinical trials drastically over-represent those from White, Educated, Industrialised, Rich and Democratic backgrounds. I hope that this continues to be a constructive tension in the coming months, which should encourage trial sponsors and investigators to make a concerted effort to engage more representative participant cohorts.

We intend to write-up these trends and tensions more fully in our forthcoming Year in Review.

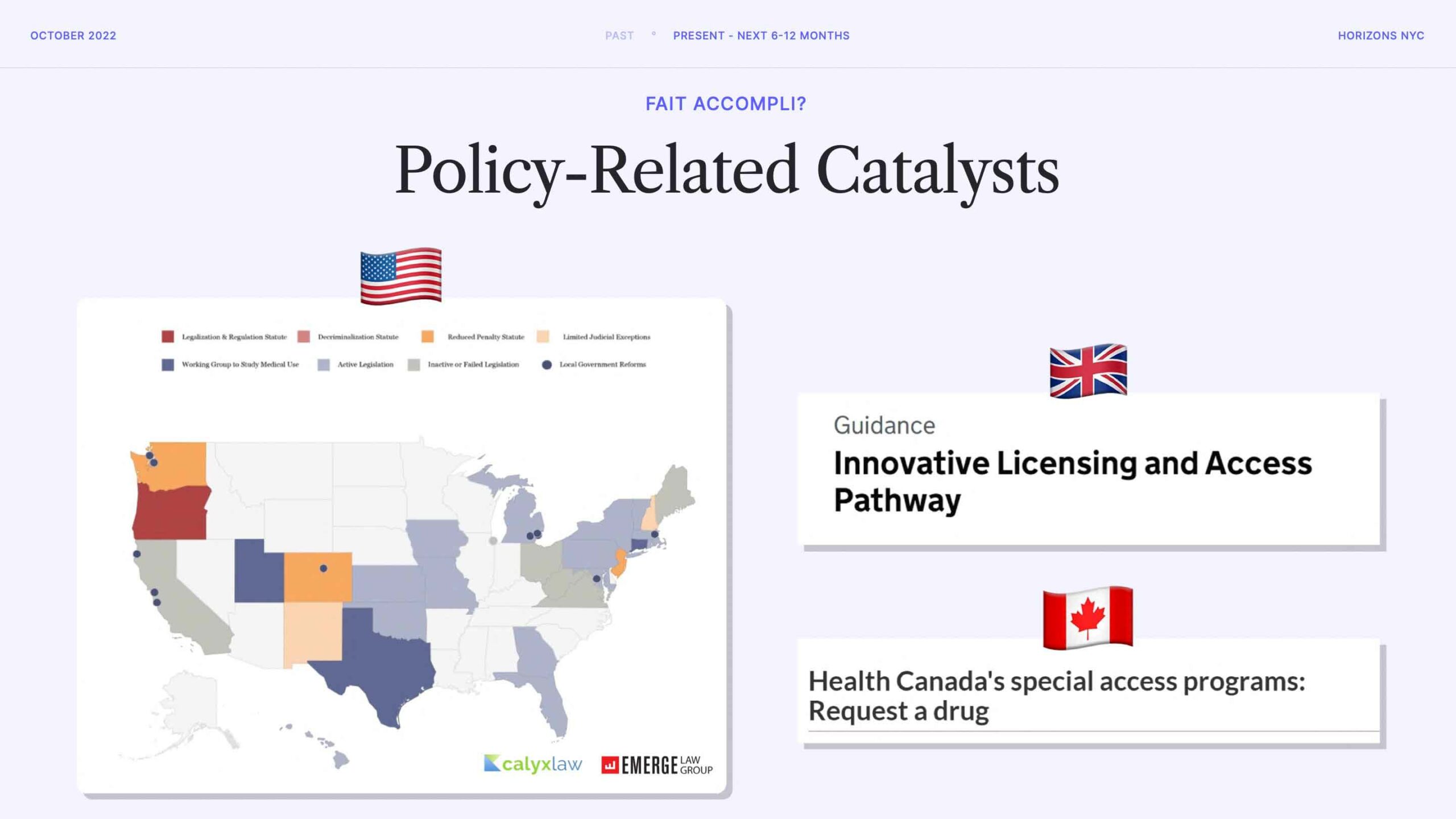

Beyond R&D, we should also expect to see further policy catalysts in the next 6-12 months. As you can see from our Psychedelic Legalization and Decriminalization Tracker, there’s a great deal of activity across the U.S. There’s also the Oregon Psilocybin Services Tracker, which keeps tabs on counties and cities that are sending opt-out initiatives to voters this November.

On that note, November will be an important month for psychedelic policy reform efforts, most notably in Oregon (where we will see which counties and cities opt-out of psilocybin services) and Colorado where Prop. 122 (which would decriminalize some psychedelics and establish an Oregon-esque legal industry) will be voted on.

Outside of the U.S., it will be interesting to see whether regulatory amendments and new drug development pathways (like the UK’s ILAP, which is similar to FDA’s Fast Track) increase access to psychedelic therapies and catalyse drug development efforts.

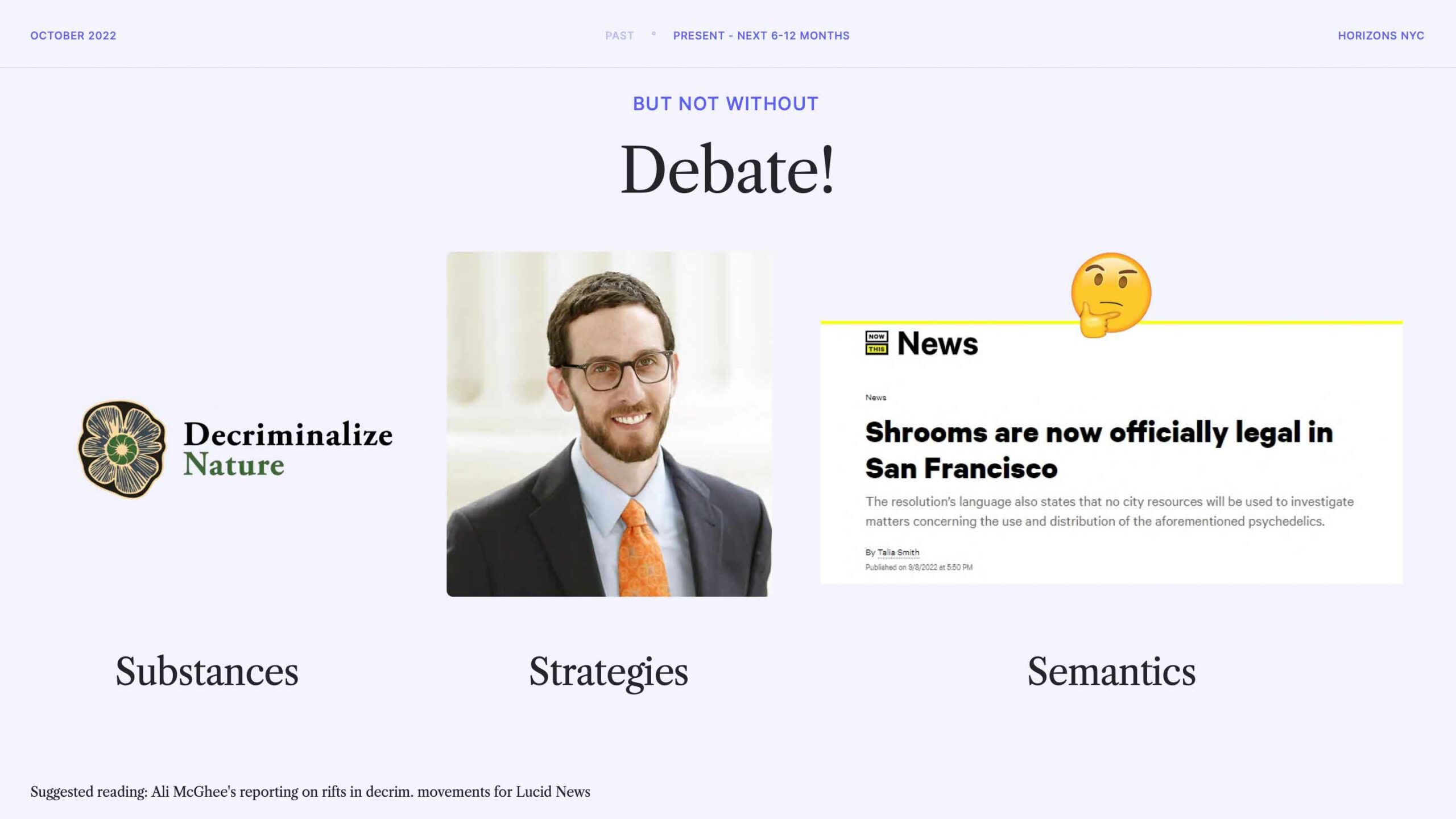

But, this policy reform won’t be without debate! And, not just from psychedelic sceptics: there’s division within the psychedelic drug policy reform movement, too. Just look at the debate around Colorado’s Proposition 122.

One example of division within the psychedelics decriminalisation movement revolves around which substances to include in such efforts. Groups like Decriminalize Nature make the case that all natural psychedelics should be decriminalized. While this seems intuitive, it belies the endangered nature of some of the natural sources of psychedelics, such as peyote from which mescaline can be derived. When coupled with the spiritual significance of such plants in some indigenous practices, it becomes ethically questionable to advocate for their decriminalization which would presumably further strain the limited natural stock of such plants.

There’s also the issue of strategies, with some efforts originating from grassroots organising and others stemming from policymakers. Pictured at the centre of the slide is Senator Scott Wiener, who forwarded California’s SB 519, a Bill that would have decriminalized psychedelics in California. Wiener’s Bill was slowly whittled away as it proceeded through the lawmaking process, and ultimately gutted and withdrawn.

Lastly, there’s the issue of semantics; it’s important to distinguish between different types of policy reform. The difference between, say, decriminalisation and legalisation is significant. If someone is led to believe that “shrooms are now officially legal in San Francisco”, as the headline pictured below suggests, they may engage in activities that run afoul of the law and end up in a sticky situation. Let’s try to be more careful in our language in the coming 6-12 months.

As my talk comes to a close, I return to this primary narrative: following a period of unabashed exuberance surrounding psychedelic research and business, critiques are now drawing focus. I think this is a natural and positive thing.

As with some of the topics alluded to in other slides, we intend to explore these themes more closely in a forthcoming Year in Review.

***

Thanks once again to Horizons for inviting me to participate in the Psychedelic Business Forum.

Miscellany

- Half of all public psychedelics companies are at risk of running out of cash this year, we shared on Twitter. According to our data, half have either already run out of cash, or are on track to do so by the end of 2022. Unless financings take place, or cash burn slows significantly, it’s the end of the road for many companies

- Is America about to enter a new era of psychedelics? Asks the UK’s Evening Standard. The piece looks at how President Biden’s cannabis pardons might open the door to a broader reassessment of drug scheduling in the states. As mentioned in last week’s Bulletin, you really should read Shane Pennington and Matt Zorn’s analysis over at On Drugs.

- The New York Times looks at psychedelic patents, but fails to reference the true prior art: Shayla Love’s reporting.

- A new review article in Nature Neuroscience explores what we know (and don’t know) about the neural basis of psychedelic action.

- The European Union’s Horizon research and innovation magazine covers psychedelic therapy.

- New suvery (N=1,801) shows that nearly half of Americans support legalisation of psychedelics for mental health, but shows hesitancy on other questions.

Weekly Bulletins

Join our newsletter to have our Weekly Bulletin delivered to your inbox every Friday evening. We summarise the week’s most important developments and share our Weekend Reading suggestions.

Live Updates

Join us on Twitter for the latest news and analysis.

Other Channels

You can also find us on LinkedIn, Instragram, and Facebook.

Join thousands of psychedelics insiders

Get the weekly psychedelic medicine briefing.

A free weekly digest covering trials, regulation, policy, and access.

By signing up, you agree to our privacy policy. You can unsubscribe at any time.